Dataloft Briefing notes address issues raised by our clients as they respond to changing housing market conditions through and beyond Covid-19.

Short term loss of rental income – how vulnerable are UK cities?

While governments across the world grapple with the personal, economic and social consequences of Covid-19, businesses need to make sense of their own short and long term outlooks.

For residential rental investors, questions arise about the continuity of rental income, volatility of demand and stability of pricing. Although much is unknown and, as yet, unknowable, we have interrogated our Dataloft Rental Market Analytics (DRMA) dataset to provide evidence of the resilience of different UK markets and provide a foundation for business planning.

We know that there has been an exodus of people from cities to more suburban and rural locations in the past few weeks and we suspect this is mainly down to students and young professionals returning to their family homes. There is a real possibility that some will choose to terminate leases on expiry and return to the city months later, causing rental voids.

In this briefing note, we address the question: how vulnerable are UK cities to short term loss of rental income in Q2 2020?

This analysis does not address the concern that student renters will simply choose to default on contractual liabilities, it is directed at the proportion of the rental market where tenants have a legal right to terminate their leases in April, May or June 2020.

What does the evidence say?

Across the UK, almost a third (32%) of tenancies are renewable in the months of April, May or June 2020. Lease start dates are not distributed evenly across the year. The busiest period is Q3 and only 13% are renewable between October and December.

In London, less than a quarter (24%) of leases expire in Q2 2020, which is significantly lower than the UK average.

The London rental market has a marked peak of activity in Q3 which, assuming the crisis has subsided by then, should protect the market from widespread loss of income.

Within London there are variations between boroughs, which seem to align with the distribution of the sharer market versus the family rental market. It is notable that 51% of tenants in London are aged between 20 and 29 – the demographic most likely to have retreated to a family home outside the city during Covid-19.

Outside London, there are significant variations between cities. For instance, in Liverpool, Sheffield, Leeds and Birmingham more than 35% of rentals are due to expire before the end of June 2020. Oxford, on the other hand is more protected with only 19% due to expire.

% of existing tenancies ending England and Wales

Existing tenancies to end April to June 2020

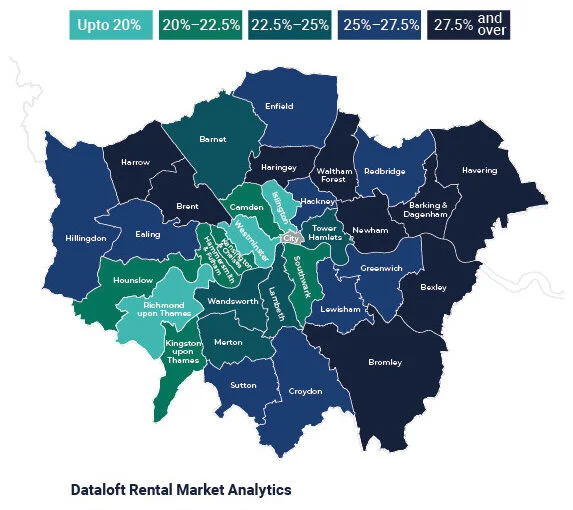

Percentage of leases expiring in Q2 2020 by London borough lower concentrations

Within London, boroughs that tend to be more popular with sharer households, are more often on the Q3 cycle and have the lowest exposure to Q2 expiries.

What does it mean?

It looks as though landlords are more protected in London than other parts of the UK because the peak in lease expiries occurs in Q3 (rather than Q2) and there is a reasonable chance of some normality having returned by then.

The London activity peak in the rental market is driven by the calendar for graduate employment starts and academic term dates. There is a real possibility that graduate recruitment will be deferred or reduced this year. It is also possible that the new student intake will be affected too, especially if overseas student numbers fall.

On the supply side, there has been an influx of supply from the short term rental market (Airbnb) which stalled during Covid-19. On the other hand, the flow of new stock from development completions is likely to slow. In locations where the peak of lease expiries is earlier, i.e. in Q2, the most likely explanation is that these markets are more aligned to the sales market, which generally peaks in Q2 before the summer holidays.

Where this is the case, although lease expiries are earlier, they may also be less exposed if they reflect a tenant base of more established households (like families with strong community ties to schools etc).

In the longer term, this raises questions about the distribution of lease expiries in a rental portfolio and the relative merits of leases that expire when demand is at its peak, versus the value of a diversified lease expiry pattern. in the short term, it suggests that landlords should be pro-active in seeking to retain tenants through this period, well in advance of approaching lease expiries.

Briefing notes in this series

Issue 1: Short term loss of rental income – how vulnerable are UK cities?

Issue 2: Short term fall in earnings – how vulnerable are UK rental markets?

Issue 3: Short term loss of overseas students – how vulnerable are UK rental markets?

Issue 4: Open market rental values – what happened to values in London at the height of lockdown?